market

Source: In Search of Alpha

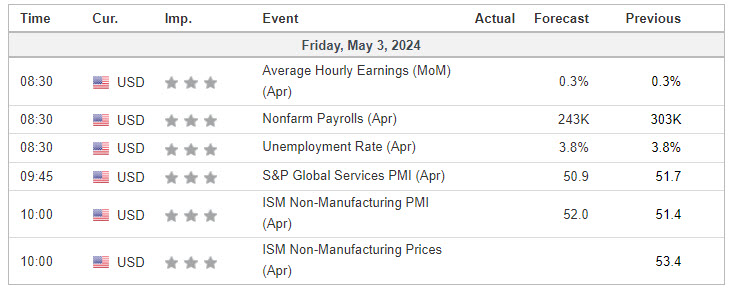

economic calendar

S&P500

S&P500

S&P500

S&P500

The previous session Cycle day 3: Following the FED Day “Range Runner” volatility session, this session retested the cycle day 1 low (5051) and bounced back safely, achieving the cycle target. The range was replaced by 76 handles in his 1.507 million contract.

…Transition from cycle day 3 to cycle day 1

this leads us Cycle day 1: A normal drop on day 1 of the cycle is 5052. Since the price ended in the top quartile of the day’s range, the bullish momentum after the close could push the price higher before the start of another decline. Nonfarm payroll is a big event today and can move the market.

As always, our tactical trade plan remains the same…staying aligned with the dominant power in Japan and China. Hence the scenario to consider in today’s trading.

bull scenario: Prices will maintain bids above 5090 and initially target the 5115-5125 zone.

bear scenario: We are keeping the price offer below 5090 and initially targeting the 5075-5060 zone.

PVA High Edge = 5086 PVA Low Edge = 5055 Previous POC = 5060

***** A 3-day cycle satisfies the positive cycle statistics 90% of the time, covering 12 years of recorded tracking history.

Range Forecast (ES) June 2024 (M)

Nasdaq 100 (NQ)

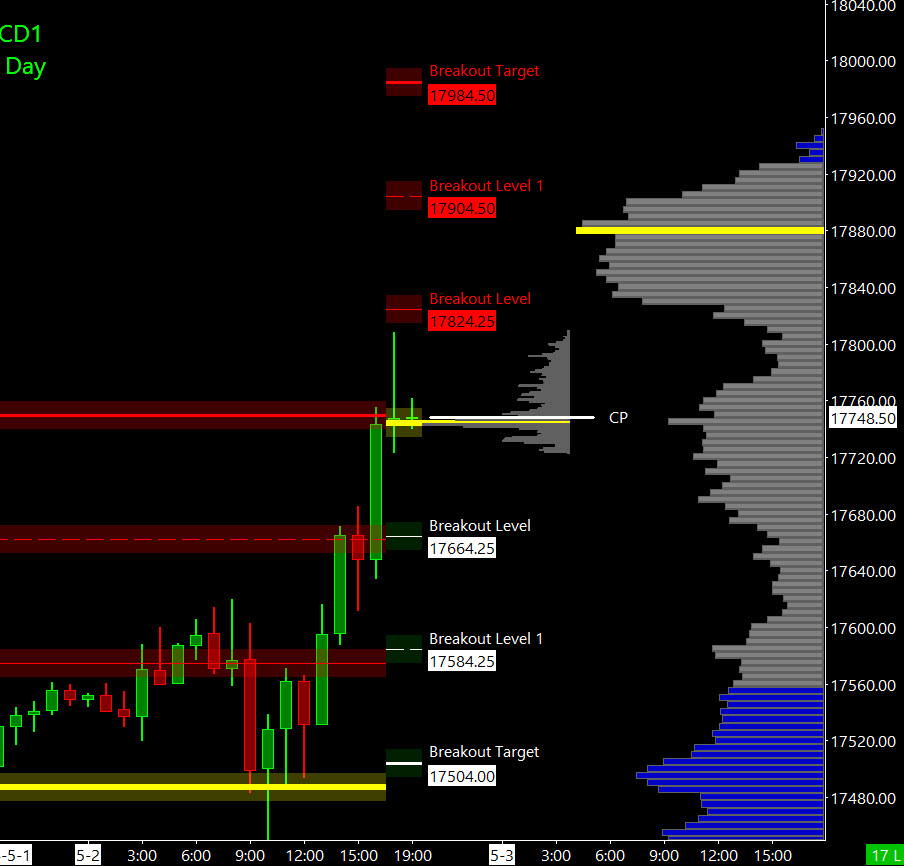

The previous session Cycle day 3: Following the FED Day “Range Runner” volatility session, this session retested the cycle day 1 low (17473) and bounced back safely, achieving the cycle target. The range of 627,000 contracts exchanged was 369 handles.

…Transition from cycle day 3 to cycle day 1

this leads us Cycle day 1: The normal drop on day 1 of the cycle is 17446. Since the price ended in the top quartile of the day’s range, the bullish momentum after the close could push the price higher before the start of another decline. Nonfarm payroll is a big event today and can move the market.

As always, our tactical trade plan remains the same…staying aligned with the dominant power in Japan and China. Hence the scenario to consider in today’s trading.

bull scenario: Prices will keep bids above 17690 and initially target the 17797-18018 zone.

bear scenario: Keep offers below 17690 and target the 17585-17535 zone initially.

PVA high edge = 17620 PVA low edge = 17482 Previous POC = 17537

Range Prediction (NQ) June 2024 (M)

Trade strategy: Our tactical trading strategy remains unchanged. Flexibly trade on both the long and short sides from your decision-making pivot level.stay focused bull/bear stacker and Premium/Discount. As always, staying aligned with the dominant forces during the day increases the probability of a winning trade.

Stay focused… Stay open-minded… Stay disciplined Always use stops.

Good deal…David

“Knowing is not enough, we must apply. Willingness alone is not enough, we must act.” –Bruce Lee

*****This trading strategy report is distributed for “educational purposes only” and should in no way be considered as a recommendation to buy or sell futures products. ”

Past performance is not necessarily indicative of future results

Important Notices! No representation is made that any profits will be made by using this strategy, system or trading technique. Past performance is not necessarily indicative of future results. There is a significant risk of loss associated with trading securities and equity options. Only risk capital should be used for trading. Trading securities is not suitable for everyone.

Disclaimer: Futures trading, options trading, and currency trading all have the potential for great profits, but they also come with significant potential risks. To invest in these markets, you must be aware of the risks and be willing to accept them. Don’t trade with money you can’t afford to lose.

This website does not constitute a solicitation or offer to buy or sell futures, options or currencies. No representation is being made that any account will or is likely to achieve profits or losses similar to those discussed on this website. The past performance of a trading system or method is not necessarily indicative of future results.

CFTC Rule 4.41 – Hypothetical or simulated performance results are subject to certain limitations. Unlike actual performance records, simulation results do not represent actual trading. Also, since trades have not been executed, the results may under- or over-compensate for the impact of certain market factors, such as lack of liquidity, if any. Generally, simulated trading programs are also influenced by the fact that they are designed with hindsight in mind. No representation is being made that any account will or is likely to achieve profits or losses similar to those shown.