Some links included here may be affiliate links, which means we may earn a small monetary bonus by referring them. This will never increase the price you pay.

How my student loan debt increased by $72,000.

From a young age, I had the idea of going to college and getting a degree. which one? Who knows, but the piece of paper was the most important thing.

When I turned 16, I had no idea what I wanted to do with my life, but I started looking for colleges. Because that’s what you were supposed to do. My requirements for the school were minimal. It had to be in a really nice location and not too difficult to get into. My confidence was pretty low at the time, but that’s about it.

After a senior trip to the Marine Institute in the Florida Keys, I decided at age 17 that I loved marine biology and wanted to attend school for marine science. I love the ocean, ships, and sea life, so I thought it was only natural.

In the end, I received a postcard from Coastal Carolina University. I applied and received my approval notice literally a week later. Talk about competitive schools 😉

They’re one of the places where you can get a degree in marine biology, and it’s located in Myrtle Beach! That’s a cool place, right?

It helped that my parents moved to Myrtle Beach when I graduated because my stepfather was opening a restaurant there. Her mother raised me as her single parent. very close That really helped me make the decision. Additionally, moving to the same state as their school meant I would receive in-state tuition.

Student loan debt begins

As I said before, my mother was a single parent and didn’t have enough money to send me to college. Student loans were pretty much my only option, or so I thought at the time.

For my first two years of college, I spent the most I could, about $14,000 each year, even though my tuition was about half that. Hello, $28,000 in student loans!

I needed money, so I started working at Planet Hollywood during my second semester. But I didn’t use any of the money I earned for tuition fees. What did you do with that? I think 90% of that money was spent on beer and eating out. But hey, I needed a social life, right?!

I knew nothing about personal finance. It was never talked about at home or at school. I remember that when I applied for the loan, I didn’t even feel anxious because the concept of debt was so foreign to me.

If I had known that I would still be paying it off in 10-12 years, I think I would have reconsidered that option.

out-of-state tuition

After the first semester, I realized that this biology study was too difficult for me and I didn’t have enough motivation to continue.

I still loved the outdoors so I decided Geography was a much better option, but Geography had more options than Marine Science. ::Enter eyeroll here::

Arizona State University is far away and I was looking forward to it, but they offered a Geography degree so it was perfect, right?

I loved Arizona, the school, the people, and everything.However, the last two years of my college career cost me out-of-state tuition. My total student loan debt totaled $72,000.

ah.

I graduated with a Bachelor of Science in Geography. Let me tell you, I still had no idea what I wanted to do with my life.

Eventually, I moved back to the New Jersey/Philadelphia area and started looking for a job. I waited in line at Red Robin Burger Shop for about six months before finding a full-time job.

I finally got a full-time job and started settling into 40-hour work weeks, learned about 401k’s, and at that point got a bit of an interest in personal finance.

But it wasn’t until I discovered the Smart Passive Income Podcast in 2013 that I learned about online marketing, online income, and blogging.

I eventually started the first version of this blog (then called Bright Cents) to write about student loan repayment.

I made great progress in paying off my loan, paying off about $30,000 in 21 months. debt report.

But after about a year and a half of just focusing on paying off my debt, some big life changes happened, including a breakup, and I realized I wanted to try this whole entrepreneurship thing.

So instead of putting all my extra money toward student loans, I started saving it.I was Save enough money for “Runway” It is also called an emergency fund, which will support you for about 8 months if your entrepreneurial venture does not go as planned.

Once you’ve saved up some money, you’re ready to venture out on your own. But as you can probably tell from what I’ve said so far, I still have student loans, and I already have them. Quit your day job.

Should you pay off your student loans before starting your own business?

How did I decide it was okay to quit before I paid off my student loans? This was a difficult decision and required a lot of thought and analysis.

The main things to keep in mind if you find yourself in this situation are:

1. Build a solid emergency fund – Have you saved enough money to cover these payments?

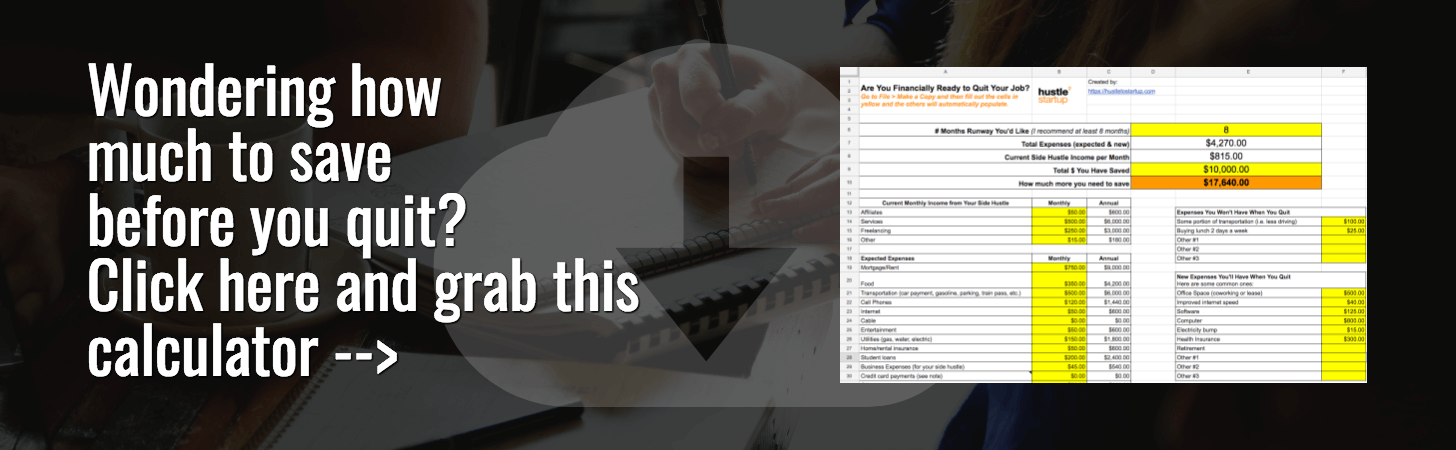

I determined how much I needed each month to pay all my bills and made sure to pay about $50 extra on top of my regular student loan payment just in case. Here’s a free calculator to help you figure out how much you should save.

I then create a separate bank account just for this money, make sure its use is clearly stated, and don’t touch the account to pay other bills unless I have to.

When I was preparing my emergency fund, I created several different accounts and tracked what each bucket of money was used for. I combined student loans and health insurance. Then, give each account a nickname to remember how much you decided you needed to save for that purpose.

I mentioned this in a previous post, but How to track all your invoices We also use the same naming convention.

Here’s how I named my account within Ally Savings.

You can only get a certain number of characters with bank account nicknames, which can be confusing for outsiders.

Basically, I needed to save $4,800 for health insurance and $2,400 for student loans. My minimum student loan payment is $200, but as I mentioned earlier, I saved a little extra to create an extra buffer, so it ended up being $2,400 instead of $1,600.

“7.2k” represents the total amount required before the account is fully completed, which is $7,200. I am still living on this account and it is accruing interest. Because, although you don’t have to dip into your savings yet, you still don’t have the confidence to get out of the bloody waters of your business.

2. Be aware of what types of student loans you have

This is an important point to consider, as some options are more flexible while others are less flexible. Here are some details about loans to consider.

Federal student loans and private student loans

If you have federal loans, you may be eligible for loan forgiveness. This means you can temporarily stop paying or at least reduce your payments for a while.

If you have a private loan, unfortunately, such an option is not available to you. This means you need to make sure you have an emergency fund and make sure you have enough savings before jumping in. Another option is to refinance your student loans. This allows you to qualify for flexible repayment terms and low interest rates.

Variable interest rate and fixed interest rate

With a fixed interest rate, you can more accurately predict your future monthly payments.

Those on variable interest rates will want to save significantly more in case interest rates start to rise again and minimum payments increase.

Do you have a joint guarantor?

If you took out student loans like most people between the ages of 18 and 21, you probably needed a cosigner to even qualify. I know what I did.

But when you’re making a decision this big, you have to take the person into consideration. If you default on your loan and are unable to repay it, your co-signer will be responsible for payment.

Don’t spoil it just because you wanted to try this.

3. How much income do you have?

If you haven’t brought the money yet, It is highly recommended that you figure out your income before quitting your day job. Without income, you will almost certainly have to dig into an emergency fund or runway for the first month. So he actually only has 8 months before he runs out of money.

For some people, it can take that long to find a job. Therefore, it may be worth resolving this issue before you take the plunge and go independent. Think about your business plan, where the money will come from, and how long it will take you to earn as much as your day job.

What to do if you start a business with debt

If you’re like me and decide you want to move toward quitting your job before paying off your student loans, there are a few things to consider.

Make additional student loan payments whenever possible

Just because you can earn your own money, make all your payments on time, and watch your income grow. Don’t think you’re out of the danger zone yet.

Until you are able to repay your loan, you should always find additional ways to pay so that if the world collapses tomorrow, collection agencies will not harass you and make your failure even more unbearable. .

The minimum amount is $200, but I’m currently paying $550 a month on my loan. I’m on a variable rate, but interest rates have already gone up since I quit my day job, so I’m trying to pay it off faster.

Make sure your emergency account is fully funded…because you never know

Sure, things may be going well at the moment, but what happens if you hit a wall or your business income declines? We strongly recommend that you always have that money set aside.

In this case, it’s better to be safe than sorry, considering that your student loan debt will not be covered if you file for bankruptcy. That’s right, you can’t let go of that ball and chain until it’s paid off.

Try not to increase expenses

I already feel like this is happening – I’m making more money so I can afford to buy this X, Y, Z tool and eat out every once in a while. However, in reality you may not yet be able to afford such a thing. I would argue that until you pay off your student loans, you can’t afford to buy anything more than what you really need to run your business.

Before adding additional elements to your business, you should focus on building a solid foundation. A solid foundation doesn’t include personal debt, so you can focus completely on one financial outcome, which is building a strong business.

Reduce personal expenses and focus on saving money as much as possible

You should look until you are debt free. how to save money Reduce expenses in all areas of your life. This includes business expenses, especially for those who initially operate their business as a sole trader. Reducing your business expenses increases your potential income.

Saving money on business expenses can also help you be more creative in translating those savings into your personal spending.

know your financial situation

All of this boils down to one thing. Are you thinking of starting a business but still have student loans? You need to be really clear about your current financial situation.

If you decide to move forward, figure out how much runway (aka an emergency fund) you need to reduce stress around money. If you have children, consider them when making this decision.

We’ve created a calculator to help you start calculating how much you should save for your runway.