How to better estimate long-term expected returns

Nobel laureate in physics Niels Bohr famously said, “Prediction is very difficult, especially when it concerns the future.” In the field of financial analysis, estimating the long-term returns of stocks over periods of 10 to 20 years is a major challenge. Accurately predicting market trends and economic conditions over such long periods of time is a major challenge, but some investors, portfolio managers, and policy makers rely on these predictions to develop effective investment strategies and policy frameworks. This challenge remains important as it often depends on Input from today’s reviewed papers provides valuable insight into how these predictions can be improved.

The paper with the straightforward name “Estimating Long-Term Expected Returns” deals with accurately estimating the long-term expected returns of the stock market. This is essential for corporate entities and individual investors alike. They investigate the ability of different frameworks and input proxies to estimate his 10- and 20-year OOS returns over long historical and more recent periods. They found that several approaches produced significant improvements compared to historical average model predictions. OOS-R2 can reach 40% even in the most recent period, and asset allocation based on the model predictions presented can improve the Sharpe ratio of a portfolio and his VaR by more than 50%. there is.

The methodology worked on by the authors runs various frameworks and proxies used to generate long-term E(R) forecasts, and compares the performance of the approaches to the expected return, which has mainly been considered in isolation. It consists of estimating the They show that E(R) can be estimated in advance for 10 to 20 years. The improvement of the out-of-sample (OOS) forecast over the historical average forecast is as much as 40% greater, even in the most recent period. The important thing is that these benefits exist within a certain period of time.

The results are of interest to those who require accurate long-term expected return predictions, and the particularly avid reader is referred to Tables 1 and 2, which provide an insightful summary of the paper’s key findings. We recommend that you refer to it.

author: Louis Ma, Ben R. Marshall, Nut H. Nguyen, Nutawat Visartanachoti

title: Estimating long-term expected returns

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4493448

Abstract:

It is very important to estimate long-term expected returns as accurately as possible. Researchers typically base their estimates on yield, growth, and valuation, or a combination of yield, growth, and valuation frameworks. We conduct a horse race on the capabilities of different frameworks and enter proxies within each framework to estimate his 10- and 20-year out-of-sample returns over 140 years and more recent periods. Our results show that several approaches significantly outperform estimates based on historical average benchmark returns, with mean squared error improvements exceeding his 40%. Using these approaches for asset allocation decisions improves his Sharpe ratio by more than 50%.

As always, we present some interesting figures and tables.

Notable quotes from academic research papers:

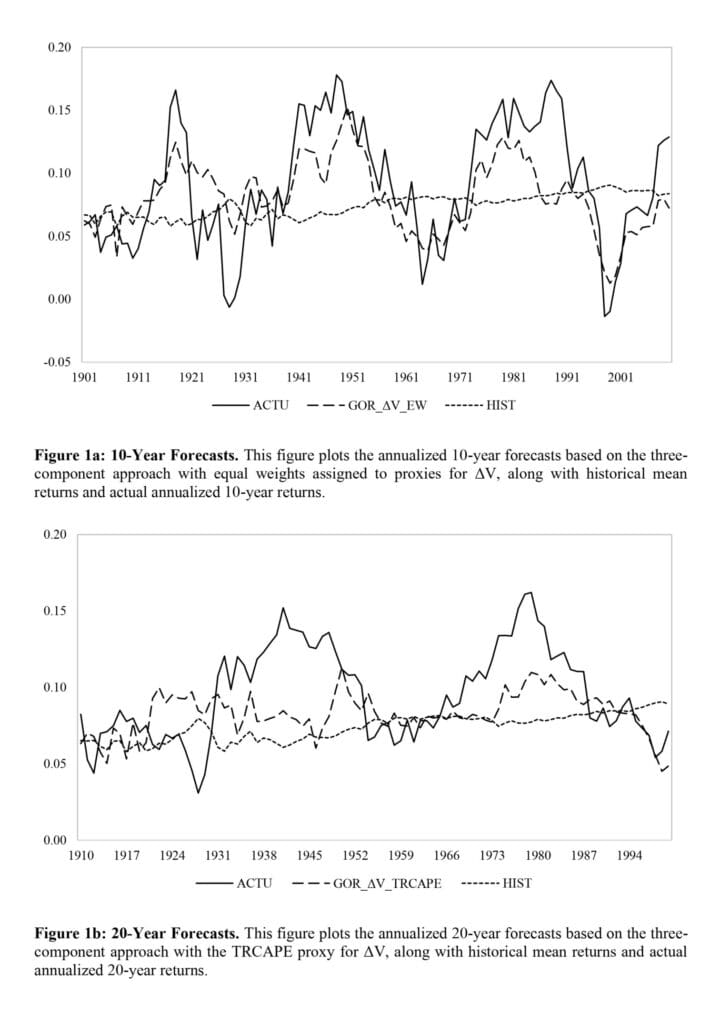

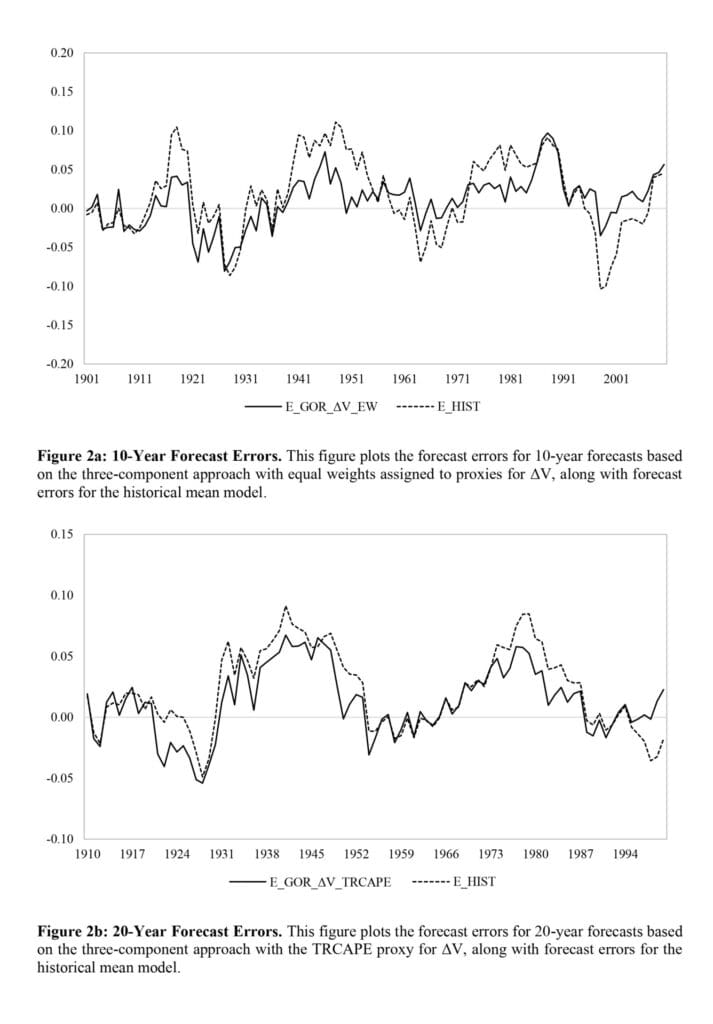

“Our results show that the three-component framework outperforms the 10-year forecast, although not by a large margin. Generating ΔV estimates based on the asset portfolio composition of Rintamaki (2023) A three-factor model (denoted by VWPC) that is not statistically different from other three-component models, such as the model that assigns equal weights to the four proxies for ΔV. This latter model performs better in asset allocation settings, so overall Considered to be superior. This resulted in a 34.91% decrease in MAE and a 57.70% increase in OOS-R2 compared to the historical average model for 10-year forecasts over the sample period 1891 to 2020 Moreover, a portfolio of stocks and bonds weighted based on these E(R) projections has an increase in Sharpe ratio of approximately 65.56% and a value at risk (VaR) of 50.06 from 1891 to 2020. % improved. Importantly, this model also leads to improvements in recent periods. 20-year returns are typically more difficult to predict. However, Total Return Periodically Adjusted Price Earnings (TRCAPE) Several approaches, such as three-factor models with proxies, can significantly improve the accuracy of these predictions.

We contribute to several strands of the literature on long-term earnings forecasting. Fama and French (1988) use a yield-only approach and show that dividend yield explains more than 25% of the variation in his two- to four-year returns. Campbell and Shiller (1998) contribute to the valuation-only literature by focusing on predicting his 10-year returns using price-to-earnings ratios derived from the average returns of the past 10 years. They suggest that it is important to consider earnings fluctuations over business cycles, and that this metric, commonly referred to as the cyclically adjusted price-to-earnings ratio (CAPE), is effective in predicting stock returns. It shows that. Bogle (1991a, b) introduces his three-factor approach and suggests that 10-year return forecasts “reproduce with remarkable accuracy the total returns actually realized.”

Table 1 shows summary statistics. The average annual returns are 10.66%, 11.76%, and 12.27% for the periods 1872-2020, 1955-2020, and 1988-2020, respectively. The returns have negative skewness over all three sample periods. Kurtosis is negative over the entire period, but positive over recent periods. Panel B shows the average geometric and log returns for 10-year and 20-year intervals carried forward by one year. It is these annualized log returns that we use in our model predictions. For a 10-year interval, the average annualized log returns for the three periods are 8.65%, 9.40%, and 8.57%, respectively, while for a 20-year interval, these are 8.73%, 9.68%, and 7.55%, respectively. Similarly, Panel C reports the standard deviation of the geometric and log returns carried forward one year at a time for 10- and 20-year intervals.

Table 2 reports the results of the 10-year forecast. MAE is calculated as the average absolute difference between predicted and actual returns. We also calculate the difference in his MAE between each prediction model and the historical average prediction.7 We measure the statistical significance of this difference using a moving block bootstrap method that accounts for time series autocorrelation. The optimal block length is determined according to Patton, Politis, and White (2009). For each predictive model, we generate 1000 bootstrap resamples and calculate the statistics based on the one-sided bootstrap p-value (i.e., the percentage of the bootstrap sample predictive model MAE that exceeds the historical average model MAE within the same bootstrap sample). Report the significance.

The results in Table 2 show that the three-component framework is the best performing framework. For 10-year forecasts, this framework has the lowest average MAE for the periods 1981-2020, 1955-2020, and 1988-2020. To see the statistical differences between the “three components” framework and the other three frameworks (i.e., “yield only,” “Gordon,” and “valuation only”), we first examine the long-term Calculate the annual mean absolute error over Utilizing the resulting four time series, we apply the Diebold–Mariano test (Diebold and Mariano, 1995). As shown in Appendix 3, the mean absolute error for “Three Components” is statistically significantly lower than “Gordon” in all three periods, and “Evaluation Only” and “Gordon” in two of the three periods. is statistically significantly lower than “yield only.” ”

Looking for more strategies to read? Sign up for our newsletter or visit our blog or screener.

Do you have ideas for systematic and quantitative trading and investment strategies? Then join us at Quantpedia Awards 2024.

Want to learn more about Quantpedia Premium Services? Find out how Quantpedia works, our mission, and our premium pricing plans.

Want to learn more about Quantpedia Pro services? Read the description, watch the video, check out the reporting features, and access pricing offers.

Looking for historical data and backtesting platforms? Check out our list of algo trading discounts.

Or follow us:

Facebook groups, Facebook pages, twitterLinkedin, Medium, or Youtube

Share withlinkedintwitterFacebookintroduce to a friend